Ready To Emanate Your Business?

"We'll Manage Your Advertising Campaigns For FREE Until You Get Results!"

Ready To Emanate Your Business?

"We'll Manage Your Advertising Campaigns For FREE Until You Get Results!"

You're a business agency pouring money into ads that reach the wrong audience. Conversions are sluggish, and your budget's bleeding. You need targeted campaigns that attract qualified clients, deliver measurable results, and build brand trust.

We are Emanate Digital, your ad-cracking, client-attracting specialists. We don't just design ads, we craft conversion

Here's how we make your business successful

Copywriting

We specialize in delivering extraordinary copywriting services, crafting compelling and persuasive content that captivates audiences. Elevate your brand's messaging with our expertise, driving engagement and conversions. Your words matter, and we ensure they leave a lasting impact.

Eye-catching visuals

We understand the power of a picture (or video) that's worth a thousand words. Our designers create stunning visuals that stop the scroll, grab attention, and leave a lasting impression.

Multi-platform mastery

We're not platform-agnostic; we're platform experts. Whether it's Facebook, Instagram, LinkedIn, Google, or TikTok, we know how to tailor your message to each platform's unique audience and algorithms.

Conversion-focused campaigns

Our ads aren't just pretty; they're designed to convert. We use persuasive copywriting, compelling visuals, and strategic calls to action to drive leads, sales, and brand awareness.

A/B testing and optimization

We don't believe in guesswork. We constantly test and refine your ads based on real-time data to ensure you're getting the most bang for your buck.

Strategic review generation

We encourage happy clients to leave glowing testimonials, building trust and social proof.

Increased leads and conversions

Watch your pipeline overflow with qualified clients eager to do business.

Social media review monitoring

We track every online mention, proactively responding to both positive and negative feedback.

Boosted ROI

No more wasted ad spend. We maximize your budget for unparalleled return on investment.

Laser-sharp audience targeting

We go beyond demographics to understand your ideal client's deepest desires, pain points, and online behavior. We use advanced targeting tools to put your ads in front of the right people at the right time, every time.

Deep audience insights

We delve into your ideal client's demographics, behaviors, and online habits, pinpointing their exact digital hangouts.

Crisis management

We're your online reputation shield, swiftly and effectively addressing any negativity.

What Our Client Say About US

"These guys are absolutely AMAZING when it comes to paid advertising. If you're looking for an agency that's attentive to details and serious about turning a $1 into $2..$3..or $4 QUICKLY then give them a try."

- Jeff B.

- Mo Mohammed with Remax.

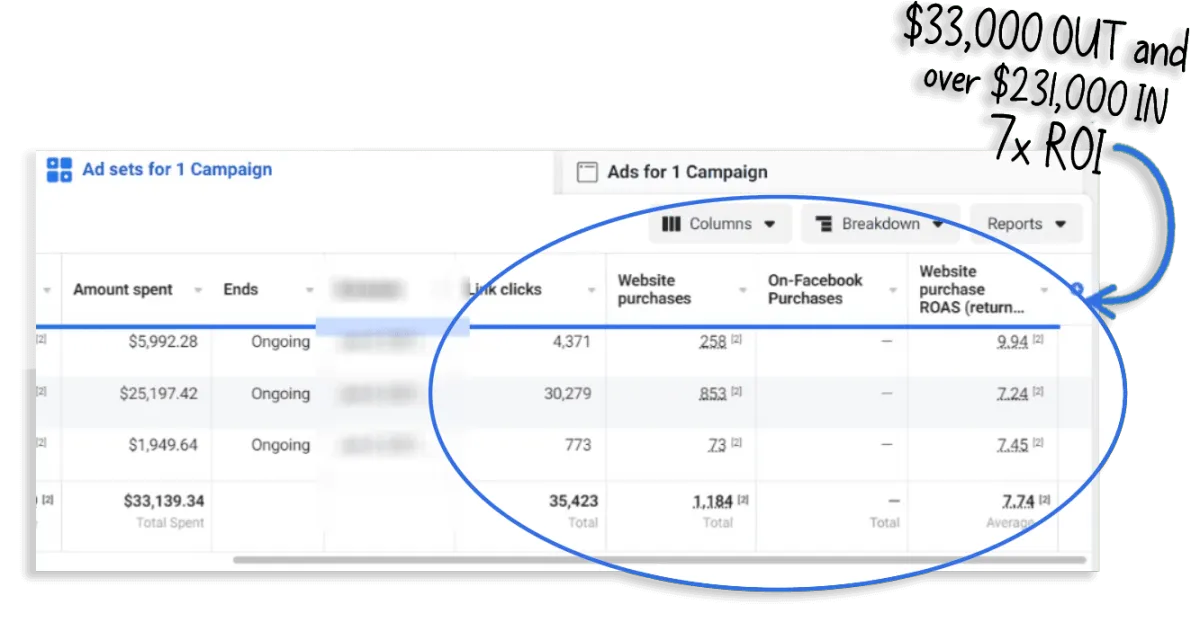

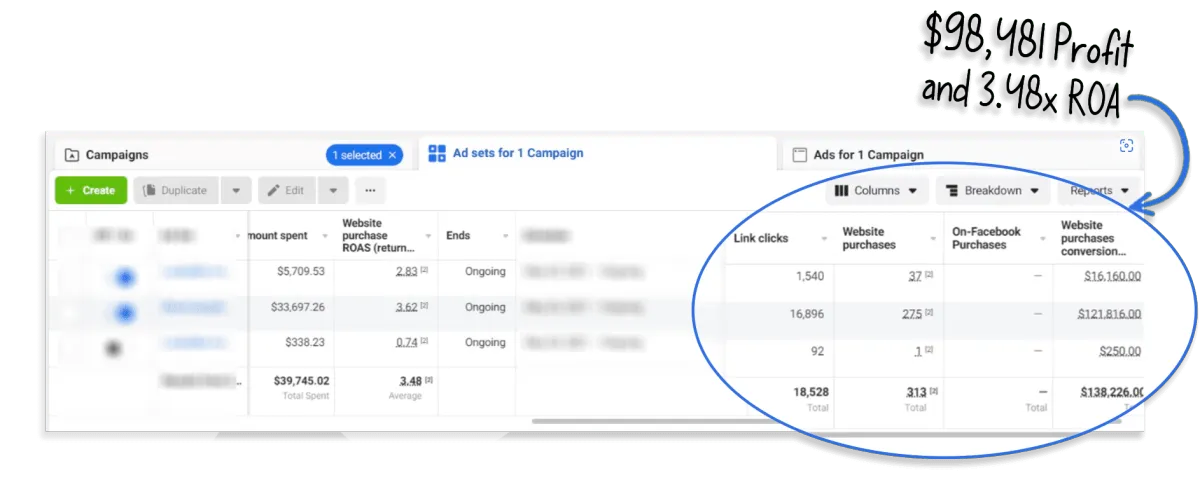

Some Of Our Campaign Results...

Discounts and Bonuses

i am giving a 30 day trial and once the trial is complete there card will be charged monthly

if they leave a testimonial video they will get 100$ reimbursed.

Benefits

.png)

Conversion Catalyst: Transform potential into profits with our ads, making you a magnet for qualified leads.

Done-For-You Ad Management: Our team will manage your campaigns absolutely free and you don't have to pay us until you're 100% satisfied.

Laser Targeted Advertising: We care about your money as if it was our own and don't waste money putting your ads in front of the wrong people.

Advance Tracking: By knowing exactly what works and what doesn't using our advanced tracking systems, this gives us a better chance of giving YOU a positive Return On Investment!

ROI Amplifier: Every dollar you spend turns into a strategic investment yielding returns with our targeting acumen.

Performance Tracker: Never miss a beat. We monitor metrics that matter, ensuring your campaign’s pulse is strong.

Budget Optimizer: Trim the fat off your ad spend, funding only the moves that move your market.

Increased sales and conversions: Compelling copywriting drives sales by capturing attention, building trust, and persuading clients to take action.

Cost-effective marketing: Well-crafted content can reach a wider audience than traditional advertising methods and deliver a higher return on investment.

Improved customer engagement: Engaging content like blog posts, social media updates, and email campaigns foster deeper connections with customers.

Stronger brand identity: Creative visuals and consistent messaging help establish a distinct and memorable brand that resonates with the target audience.

Please fill up the form

Frequently Asked Questions (FAQ's)

© Copyright. All Rights Reserved

Privacy Policy | Terms of Service